#40 - What next for property in 2023?

What I’m Listening to

The new year is almost upon us and like clockwork, following festivities, fitness will be on a lot of our minds in about a week from now. So to get ahead of the curve here is an episode from the Tim Ferriss podcast I’m relistening to with Dorian Yates (six-time Mr Olympia). What struck me about this episode is how down-to-earth he is. There’s a lot of practical advice here from one of the best which is refreshing considering the misinformation specifically in the fitness industry that exists on social media.

Resource of the week

We don’t normally think too much about our breathing but my rowing coach has been stressing that it’s important we breathe through our nose and there are new studies that mouth breathing can lead to a lot of bad things long term. So I’ve bought these nose strips that you stick onto your nose to open up the airways for my sleep, but I plan to use it for sports also. I can report that I definitely notice a difference. Will report back if there is a change in my rowing performances.

Quote

Frightened of change? But what can exist without it? What's closer to nature's heart? Can you take a hot bath and leave the firewood as it was? Eat food without transforming it? Can any vital process take place without something being changed? Can't you see? It's just the same with you-and just as vital to nature.

Marcus Aurelius

Thoughts

It’s natural at this time of year to reflect on the past year and to start planning out what’s next in 2023. There is a lot of uncertainty in the markets right now, in particular, question marks around what property prices will do next. It hasn’t helped that it’s been a pretty crazy year. We’ve had 3 prime ministers and 8 base rate rises in the space of one year and a load of back-and-forth economic policies. If there’s one thing the markets don’t like it is uncertainty.

So what next?

One big question on everyone’s mind is will interest rates continue to rise? Well technically I think it’s likely, however more relevant is how it will affect mortgage rates. Contrary to what most people think, the two are not directly correlated. When the mini-budget got announced, it induced panic in the market, investors rushed to fix rates and banks started pulling products which lead to a spike in rates leading to a sharp rise in rates. It’s important to note that fixed rates are meant to include a profit margin for banks and also their consensus of where they think rates will be at set intervals. The swap rates (the rates that financial institutions borrow money at) is lower for longer intervals meaning it’s indicating they will come down over the long term. So personally, for my products that are coming off a fixed rate, I’m in no rush to move to another fixed product, keeping it on a variable and seeing what happens in 2023.

As for house prices?

Going against the media narrative, I don’t think anything dramatic will happen. I also think the situation is more nuanced than saying what property will do in the UK as a whole.

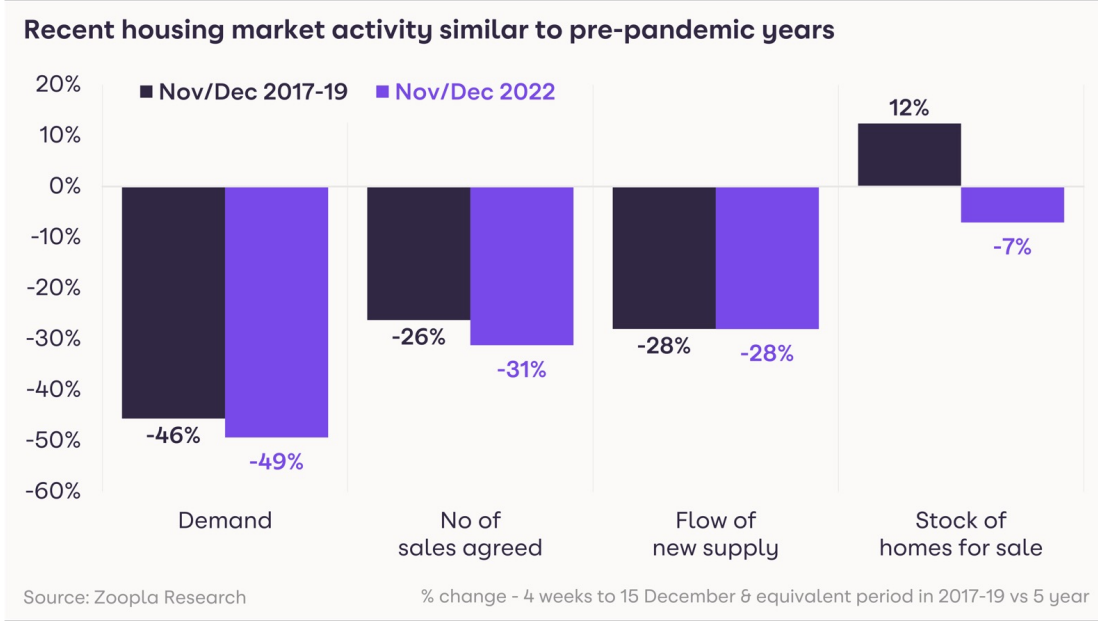

Data from Zoopla clearly shows that demand has fallen dramatically against the 5-year average, but along with this, so has the number of sales agreed. The fact is unless a seller is in a desperate position, they’ll just hold on to the property.

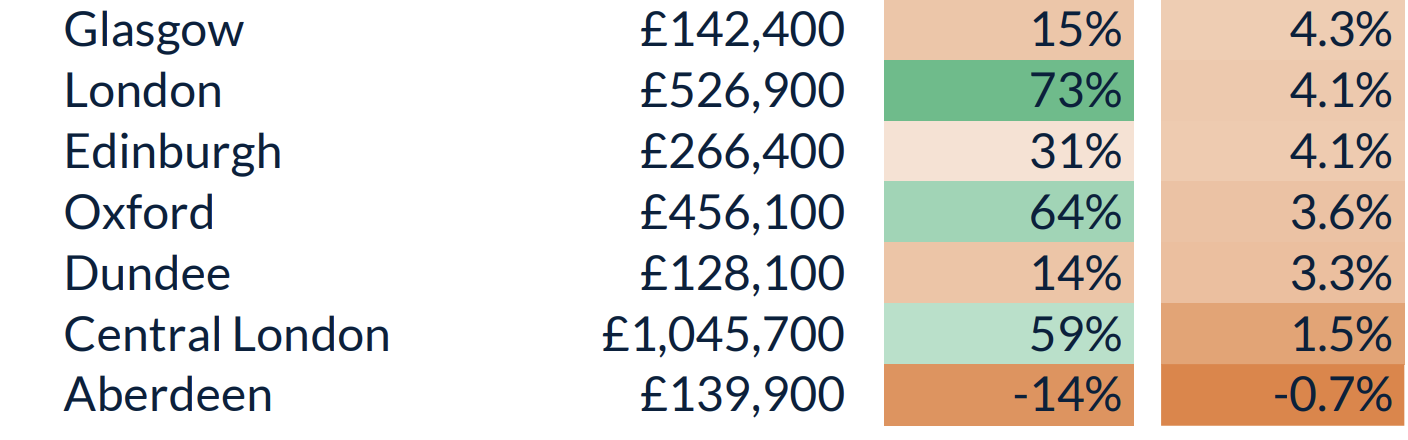

There is a huge variation in how properties perform based on where they are located in the UK.

At the top end of the scale, we’ve had properties that have grown by over 11% this year and whereas the worst has lost 0.7% of value. I think this dynamic will continue with affordability being a big driver.

Meaning that the southeast, and particularly London will struggle, especially in the buy-to-let sector as the rates squeeze out more investors and prospective homebuyers alike. Whereas we’re probably going to continue to see growth in some towns and cities in other areas, particularly the northwest.

In terms of my own investment plans, I think this presents one of the best opportunities since COVID. It has been very difficult to obtain any sort of deal in the last few years. Generally, the worse time to buy is when there is a consensus that things are going well. The current negativity means that there will be less competition and greater chance of deals being accepted below the asking price.

The way I deal with uncertainty is to have a longer-term view. It’s less about timing the market and finding the perfect investment but just to build that momentum and experience. For example if you had bought at the worst possible time in recent history, 2006 in London, today you’d still be massively up. And I think it’s extremely unlikely we’re going to see a 2007-08 magnitude crash in the next few years. I like to have that bias towards action.

So hope that sheds some light on how I’m approaching it. Hope you all have a great Christmas and catch you on the next one!

Hans